Publication of the State of The Housing System 2025

The National Housing Supply and Affordability Council says we're not on target for the Housing Accord but the target remains appropriate.

This week the National Housing Supply and Affordability Council published their ‘State of the Housing System 2025’ report. The key findings of the report were:

Dwelling prices and advertised rents continued to increase in 2024 but at a slower pace than the previous year however, both grew faster than median household incomes leading to a deterioration in housing and rental affordability.

Affordability is expected to stabilise and even improve slightly in some areas over the next 4 years.

The supply of new housing is at its lowest level in a decade with 177,000 completions in 2024, well short of underlying demand which was estimated at 223,000 for the same period.

New demand for housing is slowing and is expected to slow to 205,000 households in 2024-25 and stabilise at around 175,000 households per year from 2025-26.

The supply of social and affordable housing is expected to accelerate.

983,000 dwellings are expected to be completed during the Housing Accord period compared to a target of 1.2 million. When factoring in demolitions the increase in supply is expected to equal 825,000 which is estimated to be 79,000 dwellings fewer than underlying demand.

The Council believes that the Housing Accord target remains suitable.

Detached housing is expected to account for two-thirds of new supply over the Housing Accord period with medium and high density volumes expected to remain low compared to the previous decade.

Cyclical constraints to supply are easing.

Structural constraints remain the principal barrier. This includes things such as a lack of skilled workers, scarce, fragmented and costly land for new development, low productivity, restrictive and complex land use and planning approval systems, market frictions and financial incentives that limit optimal use of current housing stock and fragmented housing policy which impacts on delivery.

The Report also had five policy recommendations which are ranked by priority and detailed below.

Increasing investment in social and affordable housing through proven mechanisms, and reviewing regulatory frameworks for the social and affordable housing sector

Improving construction sector capacity and productivity

Applying best practice principles to planning systems and ensuring developable land is made available

Supporting better outcomes for renters

Ensuring the tax system supports housing supply and affordability

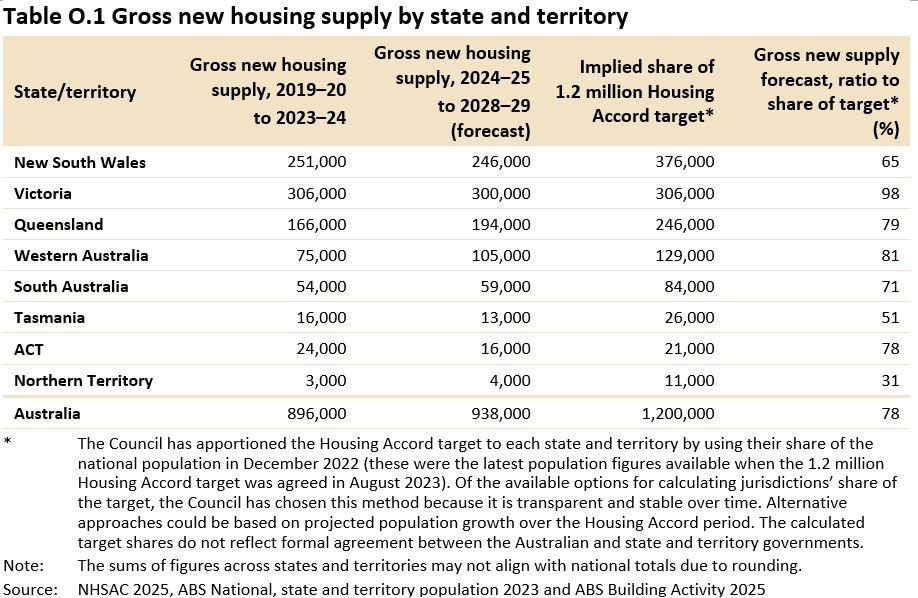

In terms of the expected volume of new housing delivered during the Housing Accord period and how it compared to the target, the table below details these figures.

As you can see, not one state or territory is expected to build enough new housing to reach the Housing Accord target. The target is supposed to be challenging and Vic is expected to go quite close (98%) with WA (81%) and Qld (79%) also expected to go relatively close while NT (31%), Tas (51%) and NSW (65%) are expected to end up the furthest away from target.

Key takeaways

The Report shows that we are currently not on target to achieve the Housing Accord target. Given this was a target that was developed by Labor and they have retained government with an increased majority they should be pushing much harder to lift new construction as soon as possible.

We should also be aware that the estimates of underlying demand for housing are predicated on government forecasts for population growth which at this stage are looking unlikely to be met.

The big thing that is missing from this report is the actual estimate of the current undersupply of housing which is very disappointing. If you are going to write a detailed report about the housing system and volume of housing required, a good starting point would seem to be establishing what the current shortfall of housing is but this report has failed to do that.

Now for the good news. The escalation in construction and material costs is easing and interest rates have now been reduced by 50 basis points and are expected to fall by at least another 50 basis points this year. The lower financing costs and the greater surety on construction costs should see an improvement in new housing delivery. In fact, dwelling approvals are already starting to trend higher, albeit they remain well below levels required to achieve Housing Accord targets.

There are still challenges to delivering more housing such as the cost relativity between new and existing properties particularly in higher density markets of Sydney and Melbourne. The increasing time it takes to build properties is also a key challenge and a big part of the reason the Housing Accord target is unlikely to be achieved.

Higher density can deliver more housing but it takes longer to complete so if the Government wants to achieve the ambitious target they have put in place, they will need to double-down on incentivising and approving new houses in particular. This is because they can be delivered faster and at relatively lower developer risk than higher density product. We shouldn’t neglect higher density housing but realistically if these projects were going to be built before mid-2029 they would need to have started by now.

I’d love to hear your thoughts and comments.